TRADING WITHIN THE TREND

Now that we have looked at trend definition, the next thing to do is determine how to take advantage of the current trend. Of course, the Basic Trend as defined in the previous article provides a strong backdrop from which to build further and, for some at least, may be enough to complement their short-term trading ideas. As a standalone indicator (derived from a back-tested strategy) its potential as a trend timing tool is evident and may be used on its own. However, for those who trade more actively, it will be worth looking at our mean reversion strategies. These are effectively just small, potentially more reliable segments of the greater ‘Basic Trend’ which we simply call TrendBytes.

The previewed ‘RSI’ strategy overview provides a good example of a simple entry and exit strategy, within a primary trend. Like the ‘Basic Trend,’ the TrendByte methodology uses multiple reversion type strategies to create our ‘composite’ mean reversion barometer for both SPX and NDX (combined multi-strategy overview), as well as a ‘single’ strategy for each index which provides a simple short term ‘positive,’ ‘negative’ or ‘neutral’ reading. These are all based on back-tests dating back at least 15 years to capture as many trend types as possible. As mentioned, there is no guarantee that these will perform with the same accuracy in the future, however, the intention is to use these as focal points from where a technical view may help to support either a similar view, or otherwise.

To ascertain whether our TrendByte strategies have been historically viable or not, there are certain basic things we are looking for:

- A robust equity curve which will be indicative of past persistent positivity

- Low drawdowns (Particularly as a proportion of net profitability)

- A balance between long and short positions within testing (This is important, especially given the positive directional bias that has prevailed over the past decades for the sake of balance)

Note that, unlike the ‘Basic Trend’ strategies, these strategies are short term in nature with a short holding period through testing, normally 3 days or less. As such, these may be more suited to those who have time to monitor markets more actively. These are not trend indicators, but short-term reversion techniques.

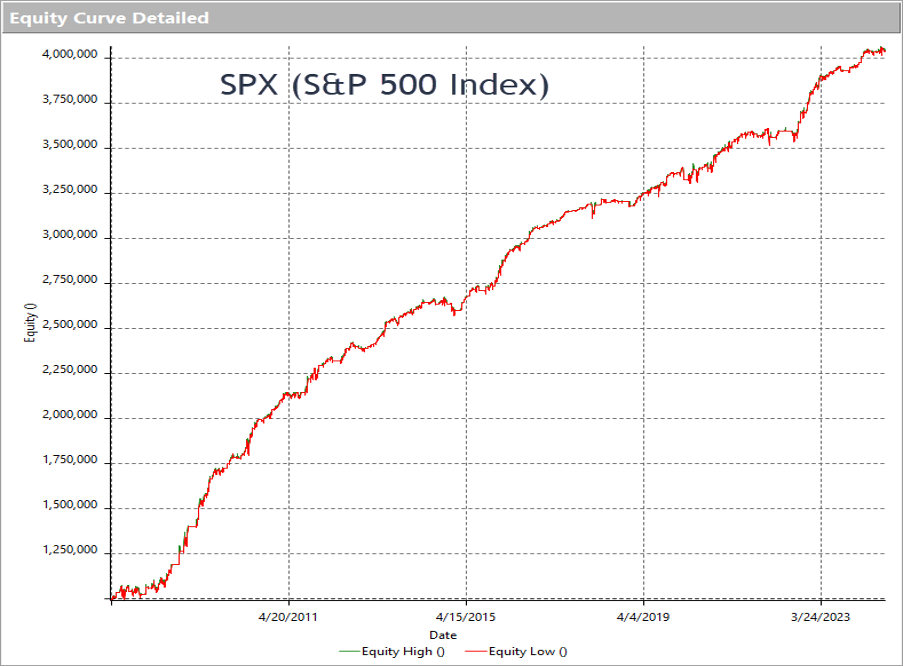

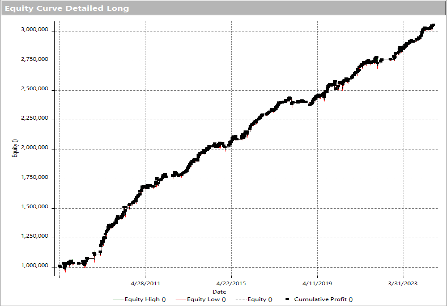

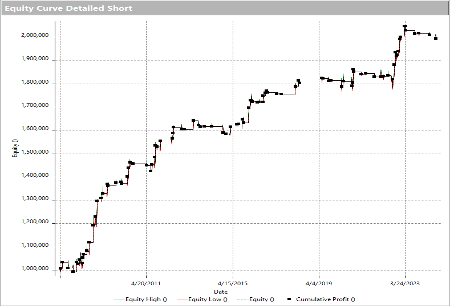

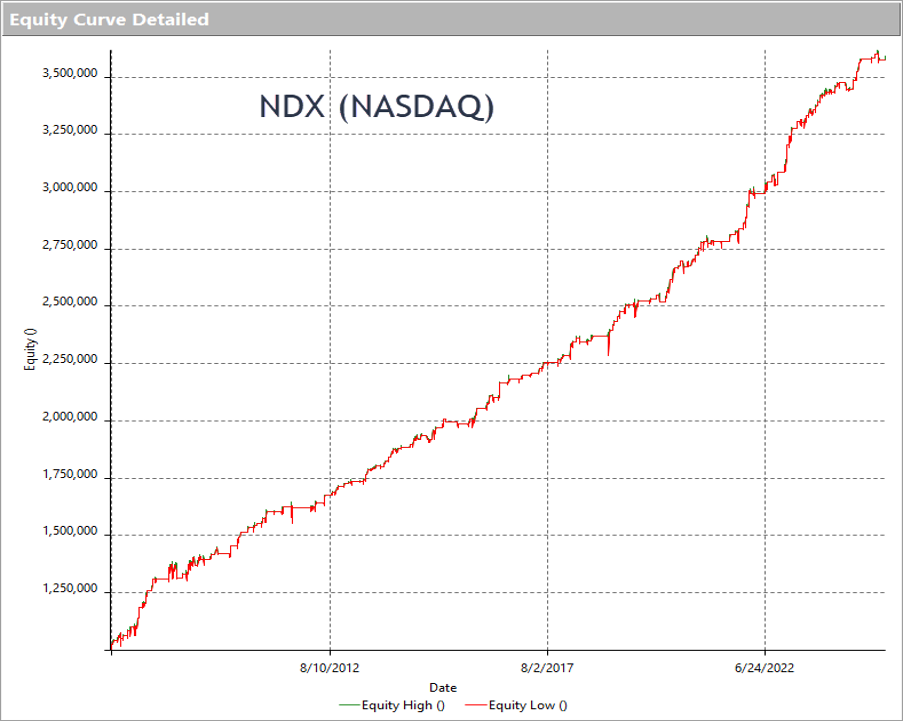

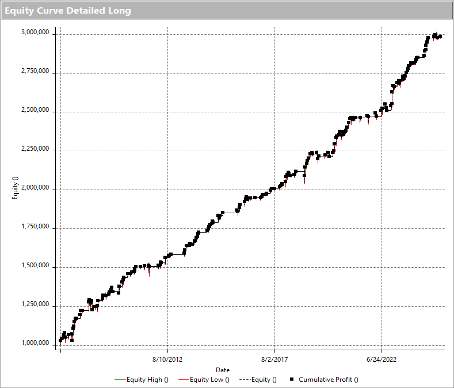

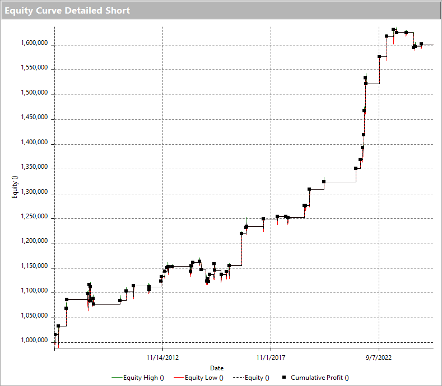

Equity Curves SPX and NASDAQ

For the single TrendByte strategies when applied to the S&P 500 and NASDAQ, please see the graphs below.

Percent Profitable = 75.14% Net Profit / Drawdown =29

Although the Long trades were more plentiful because of the index bias during testing, the short side remained positive throughout.

Percent Profitable = 78.04% Net Profit / Drawdown =25.7

Similarly, the long performance is more solid given the market situation, however, short side trades were firm and consistent over the testing period.

Daily updates will be provided for both ‘Basic Trend’ and ‘TrendByte’ strategies within the U.S. Index sections – Both composite (multiple approach) and a more binary and simple single strategy for S&P 500 and NASDAQ indices. As standard, technical overviews will verify statistical output.