EQUITIES & PORTFOLIOS

Many of the previous articles to this point have focused on the first aspects of market timing when specifically applied to an index. As mentioned, although the index itself is not technically a tradeable asset, there are many ways to trade the index valuation whether through futures contracts, ETF's and other etc. In many ways, an index is essentially a type of portfolio containing multiple stocks in variable sizes which is the reason why there is inherently less volatility in an index when compared to a single stock or equity. The averaging effect of multiple levels of performance dampens the excesses of outlier extremes.

To see what is in the members area within the equities section consider a free trial to better understand the daily output to help start your day with solid preparation. Let us consider some recommendations on how best to start and manage this process. Remember, within the context of our prep plans, back tested portfolios are treated as indicators. In other words, forward-looking directional preferences from a back tested portfolio are not to be considered without additional visual oversight. The TrendPrep approach is to use Information generated through testing as focal points or points of recognition where a stock may be considered to have potential skew based on historical theoretical performance. Where the back tested decision is aligned with the users (helped by the online technical insights provided on this site), it might add some confidence around the decision of whether to participate at this time, or not, and in what direction. Some considerations -

- At the outset, it is sensible to create portfolios which are not too large. This will help to familiarise amalgamating Statistical data output with technical oversight. Like anything, practise makes perfect. The portfolio we use is simply the largest 25 capitalized stocks in the US market.

- Keep all positions at the same size. This creates balance among decisions and simplifies the process. Position sizing can be added later but, for the purposes required at the initial stages, this is more of a complication and may cause confusion. Each decision is as important as the next.

- The benefit of creating such balance is that the risk on each single decision made is, for better or worse, diluted effectively. Within the context of a 25-stock portfolio, A 10% drawdown on a single stock is effectively relative to a 0.4% drawdown within a portfolio. Of course, the opposite naturally applies on the benefits side of things. When individual decisions have a lesser weight in the context of ‘ruin’, making such decisions becomes less stressful. It is important that trades entered in to are less emotional and based more on the balance of probabilities, having weighed up all the evidence.

- Again, on the topic of balance, it is also a positive to have a solid representation of trades in both directions (Long and short). Markets can have multi-year trends which then suddenly turn. The norm for equity markets in recent time, particularly those in the US has been for low volatility growth with the occasional higher volatility dramatic retracement. Therefore, it would be quite easy to create a profitable strategy which has many more long trades than short trades. The problem arises if (or when) markets decide to about turn. The portfolios presented in the equity members area will all have a focus on these aspects surrounding balance i.e. similar numbers of long and short trades, as an example.

- In addition, the target is to, wherever possible, have similar annualized performance and achievement metrics. Consistency and balance in back testing are crucial as they represent numeric barometers that gauge performance in multiple ways. This then allows forward monitoring. If current metrics deviate significantly from the historic theoretical metrics, then action can be taken to remediate and adjust where required.

- Always remember, consider the historical back tests, either for index or portfolios, as indicators. The historical representations may be indicative of future performance or not. Either way, it is preferable to use something that has historical context for guidance purposes. Whichever indicator you may currently use, if it does not have solid balance and timing when applied to past data, it is of little, if any use.

UNIVERSAL and OPTIMAL PORTFOLIOS

At the outset, we will look at two portfolios using the ‘US 25’ large cap stocks. Both will be updated daily for those who have membership to the equities section of the site, and for those with an initial free trial.

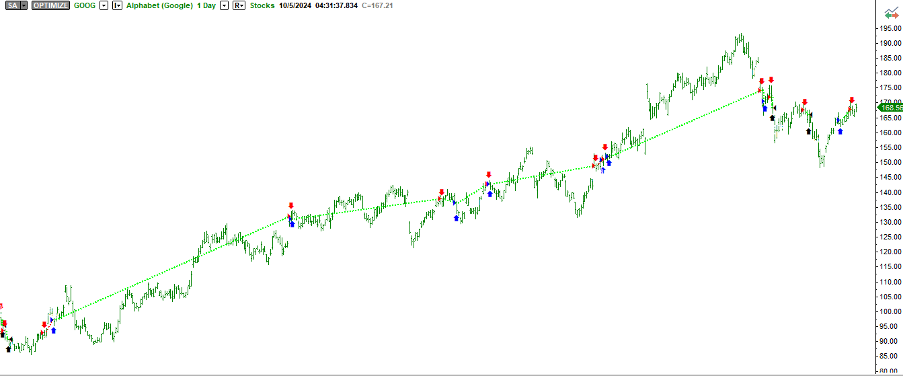

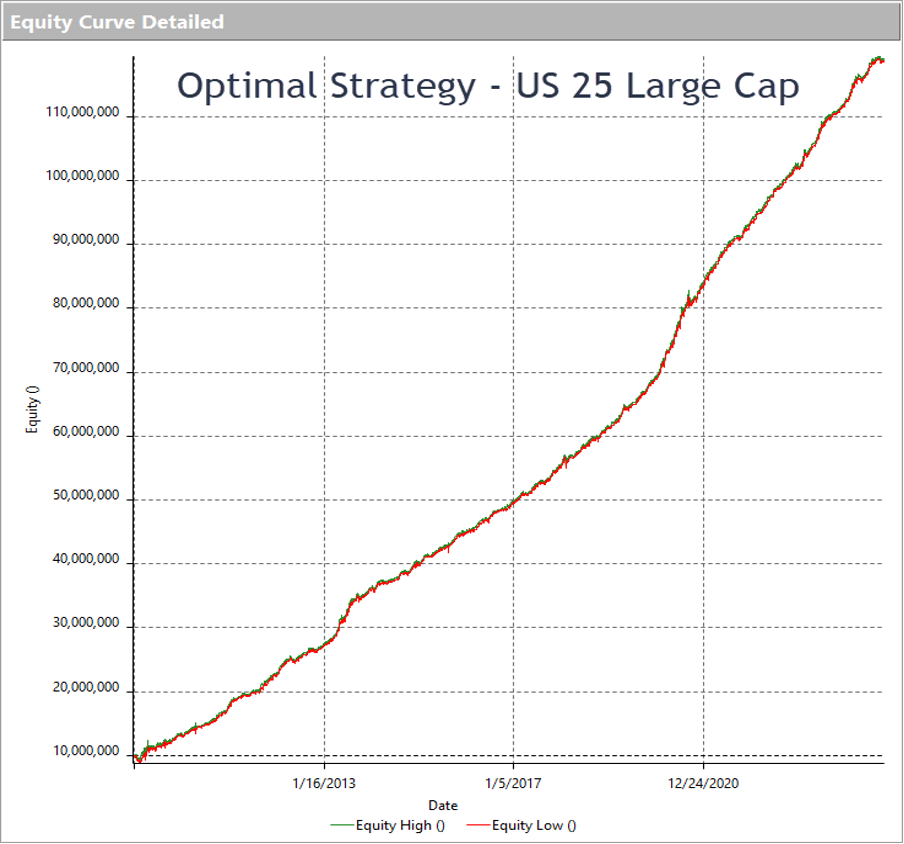

Firstly, The ‘Universal’ portfolio. In simple terms, it uses the same logic as the Basic Trend strategy applied in the Index section, and it uses identical parameters for every component of the portfolio. It is effectively a ‘one size fits all’ approach and uses price data alone for the decision-making process i.e. no fundamental, volume or external data is used. To get a sense of how it may look when applied to a chart, we have attached the graph below as a visual representation.

To see how the UNIVERSAL strategy stacks up against the criteria set above there are some tables added below with some very brief commentary.

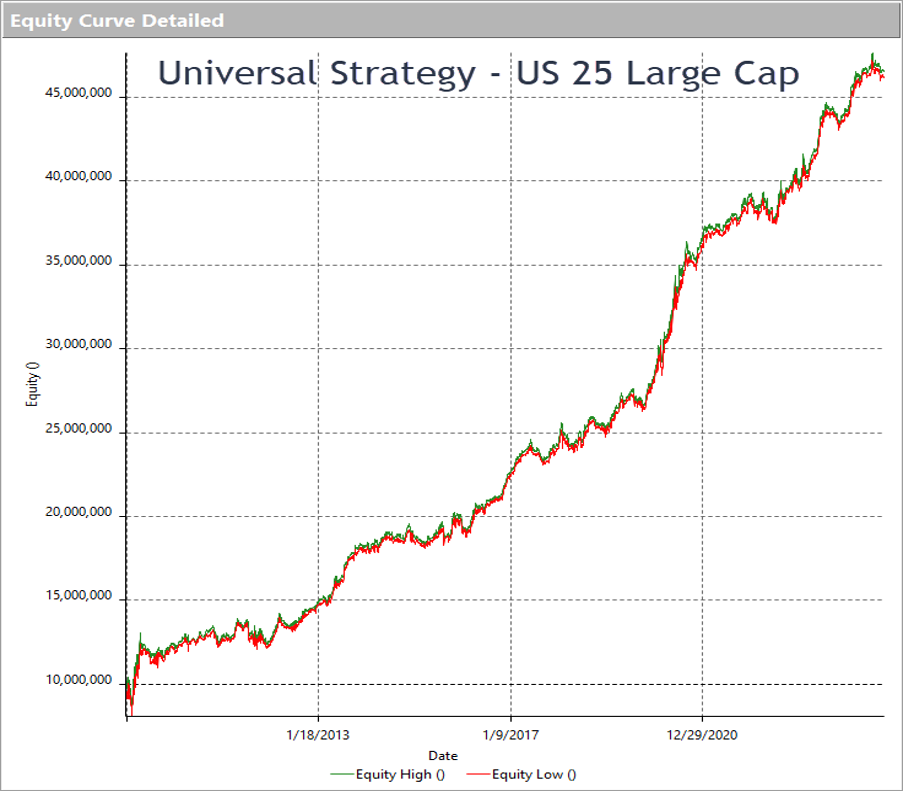

This is a view of the equity graph over the testing period which, given the static nature of the ‘one size fits all’ approach, is quite promising. What’s more, the other metrics satisfy our requirements for balance and consistency below.

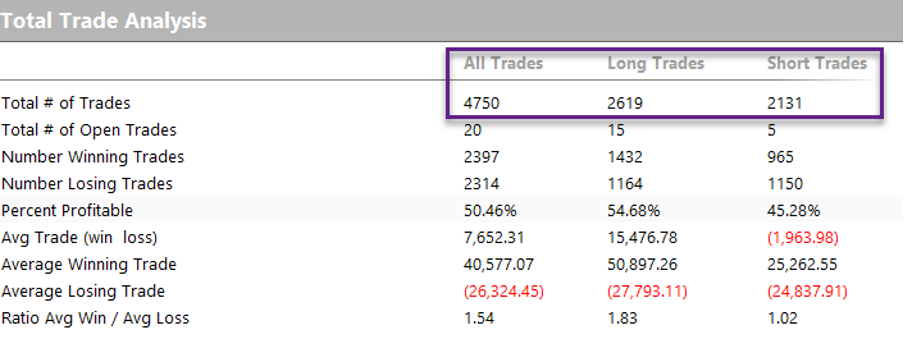

There is a reasonably good balance between the number of long and short trades which, given the bullishness of the testing period shows balance, however, the short trades lost money because of the constant market strength.

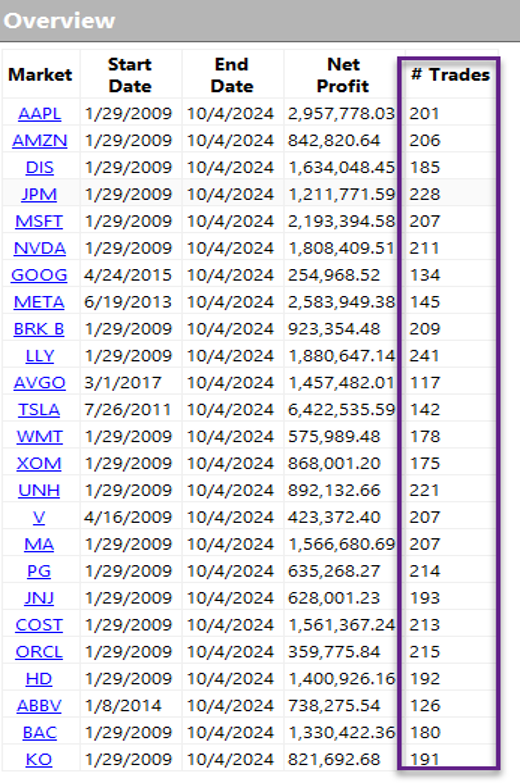

As the table above shows, over the test period, every single constituent had a profitable return and the number of trades for each were consistently in the same region.

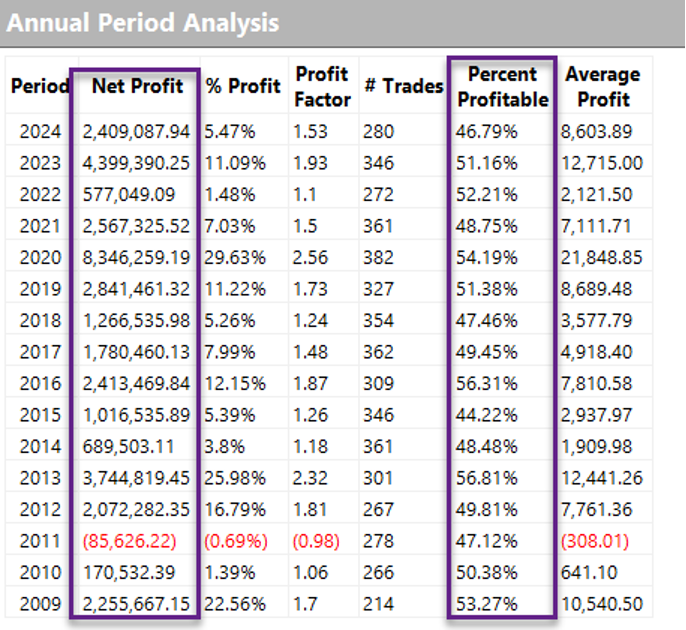

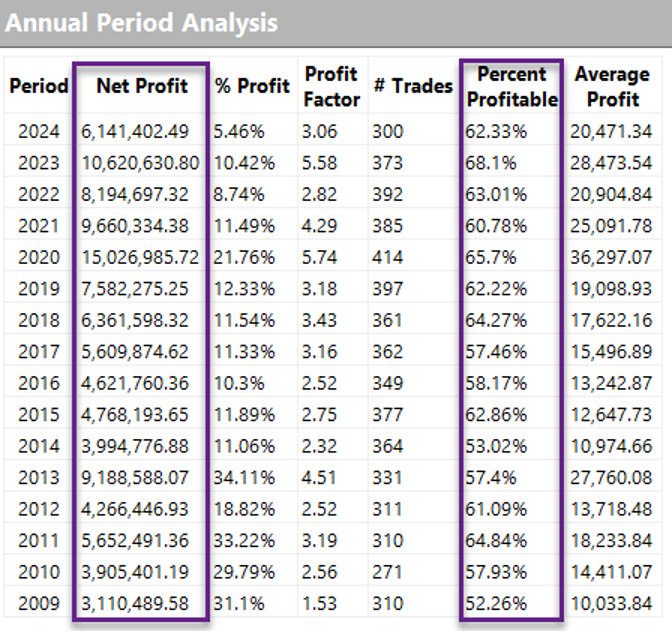

Finally, the percentage of profitable trades was consistent throughout, and all years (with one exception) proved profitable. In its entirety, this strategy meets all the criteria required and, although it is impossible to predict the future, the nature of statistical consistency allows for us to monitor whether general performance remains on track or if there is any degradation. With the visual technical overview complimenting this approach, there is every chance to maintain this consistency beyond this point.

Next, we will look at the OPTIMAL portfolio. The difference between this portfolio and the last is very simple, but the consistency requirements remain the most important metric for future monitoring and use. Each component has been optimized to ensure a robust equity curve. There is always discussion regarding ‘over optimization’ and whether the past may be representative of the future. Firstly, the answer is that it is impossible to know, however, given that each decision has a technical visual overview for validation, and the back tests are considered as an indicator or reference, then optimization will be used. It is important that indicators have some historical context and validity,otherwise why use them in the first place. Indicators that have not passed back test scrutiny are of limited use. Optimal solutions can signal possible forthcoming directional changes. Visual technical validation and the monitoring of historical metrics are either utilized to support current back test view, or to alert to changes in historic patterns.

This equity curve is very impressive as might be expected to some extent when each stock has been independently optimized and may be too close to perfection if used on a standalone basis. However, this will be used as the indicator and alert system and subject to further oversight, as well as observed for notable behavioural changes. Below are tables for the consistency elements which will need to be monitored going forward.

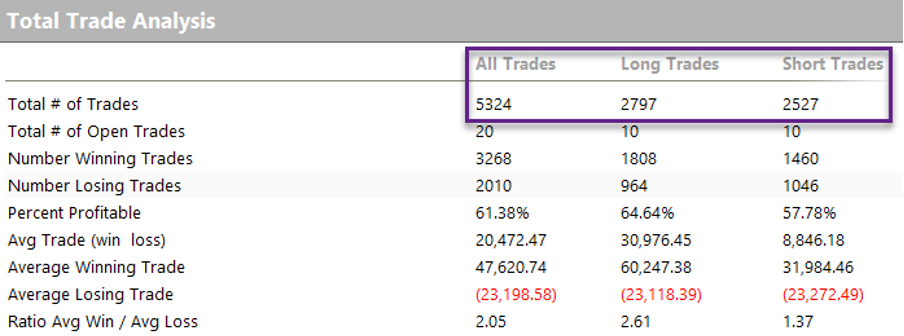

The number of long and short trades suggest a reasonable balance, though this time the short trades have been more positive than with the Universal approach. The same is true of Percent Profitable and other metrics.

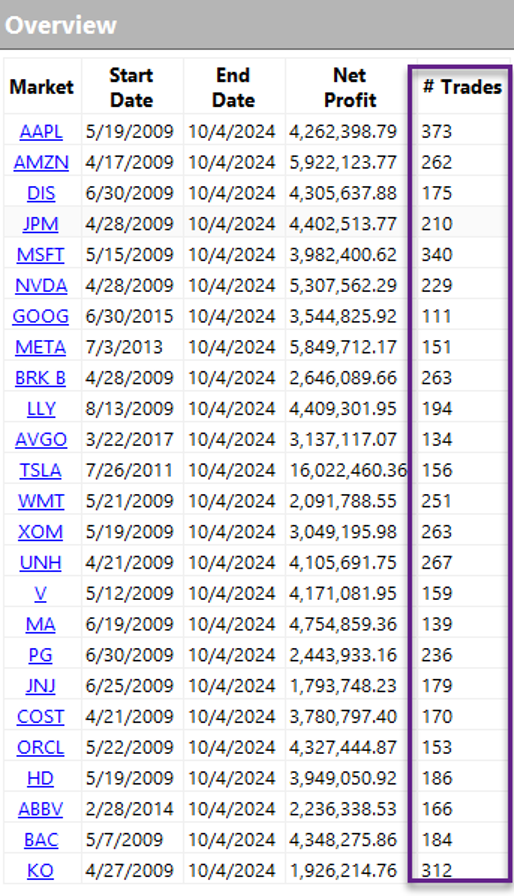

The number of trades has been generally consistent over the period but, once again, every stock has been profitable. Though, given that each has been optimized, this is entirely expected. Nonetheless, this provides further data going forward as a measure of whether the future has remained consistent with the past.

Finally, Percentage of profitable trades have been consistent, and each year of the testing period has been positive. This forms a sound and strong statistical footprint for future decision making.